Fintech Singapore: The Fastest Growing Industry and What You Should Know About It.

Wilson • May 26, 2016

Wilson • May 26, 2016 Don’t say good things bojio.

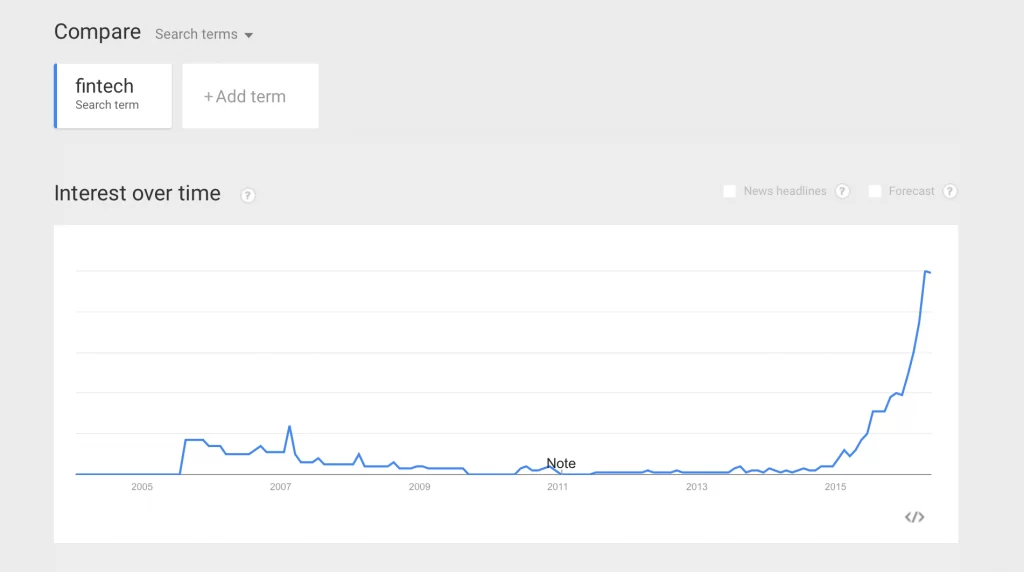

Google Trends indicates that interest in fintech Singapore has shot up more than 14 times since 2015. This could also means there are more fintech jobs in Singapore.

Fintech is an extremely hot topic of interest in both the finance and technology sectors.

However, if you haven’t already realised, resources, information and ideas about Fintech are highly coded by jargons and existing contextual knowledge.

So this week I have tried to write about Fintech, bite sized, and I hope that the article will be useful for you!

Fintech, or Financial Technology, is an initiative carried out by tech companies to digitalise financial activities. It is heavily funded by investors (billions of dollars) and many big names swear upon it.

Recent article from New York Times, featuring Fintech investors from Wall Street.

Fintech industry research performed by big names PwC, McKinsey and Capgemini.

Tech companies are now developing tech products (softwares and applications) that allow users to perform all kinds of financial activities at the tap of their mobile screens.

Financial activities include:

- Lending

- Payments

- Investments

- Personal finance management

- Foreign Exchange

- Crowd funding

- Financial analytics

and many more.

This means that actions like:

- Calling or going to the bank/financial institution to apply for a loan or buy a share

- Keying in credit card numbers to make payment

- Opening several bank accounts and sorting them as savings, current or foreign

- Paying hefty amounts for analytical softwares

are becoming obsolete.

Take note: banks and financial institutions are not becoming obsolete, but traditional ways of performing financial activities.

Softwares and mobile apps are replacing professional services and physical sites. Now, all we have to do is download an app or create an online account, and we can get all the services we need. We can avert the hassles of taking a queue number, being put on hold, or going through mountain piles of paper work.

Enough said, let’s take a look at three Fintech companies in Singapore:

1. Numoni

Mission: to empower the Global Underbanked with F.A.S.T.™ Payments.

(Future & Forward | All & Any | Safe & Secure | Through & Transformative)

Vision: to become a Bold Sustainable Enterprise empowering 100 million people with $1 a day.

Numoni was founded in 2012 to enable cashless payment methods for unbanked populations.

It has 6 transaction platforms:

(1) Recharge platform

Nugen users can:

- Add minutes to their prepaid mobile phone cards (recharge prepaid airtime)

- Top up prepaid vouchers to shop on-line securely (recharge prepaid vouchers)

- Reload electronically stored value voucher (recharge stored value wallets)

(2) Remit platform

Nugen users can:

- Remit prepaid airtime, vouchers and stored value wallets for families overseas

(3) Repay platform

Nugen users can:

- Repay monthly recurring bills such as utilities bills, automotive bills, monthly subscriptions fees and microloan repayment

(4) Release platform

- Dispense local currencies from rebates, refunds and disbursement of donations

(5) Receive platform

- Collect micro-savings and donations for any charity drives

(6) Retail platform

- Purchase games credits, discount vouchers, issuance of entrance tickets

These transaction platforms make Numoni’s products worthwhile buying:

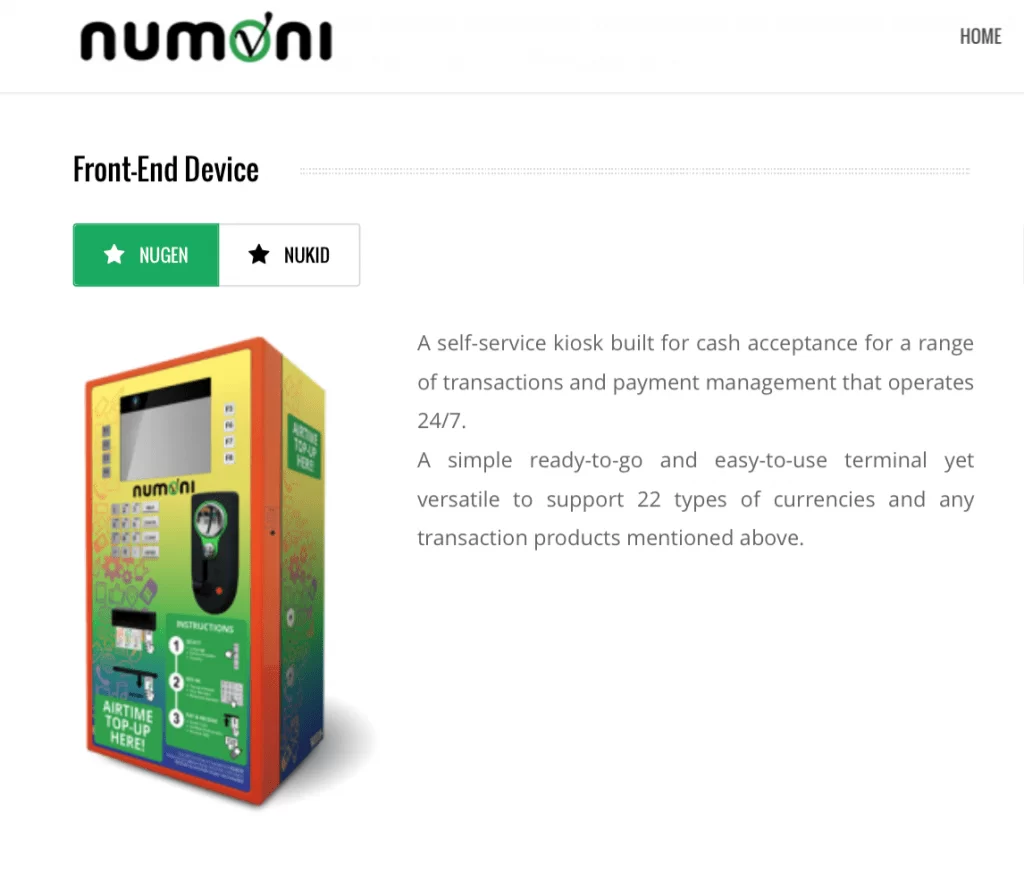

#1 NUGEN

This is Numoni’s main product, an ATM-like terminal.

This simple self-service terminal enables micro remittances, micro payments and micro loans. And by micro, I mean amounts like US$1.

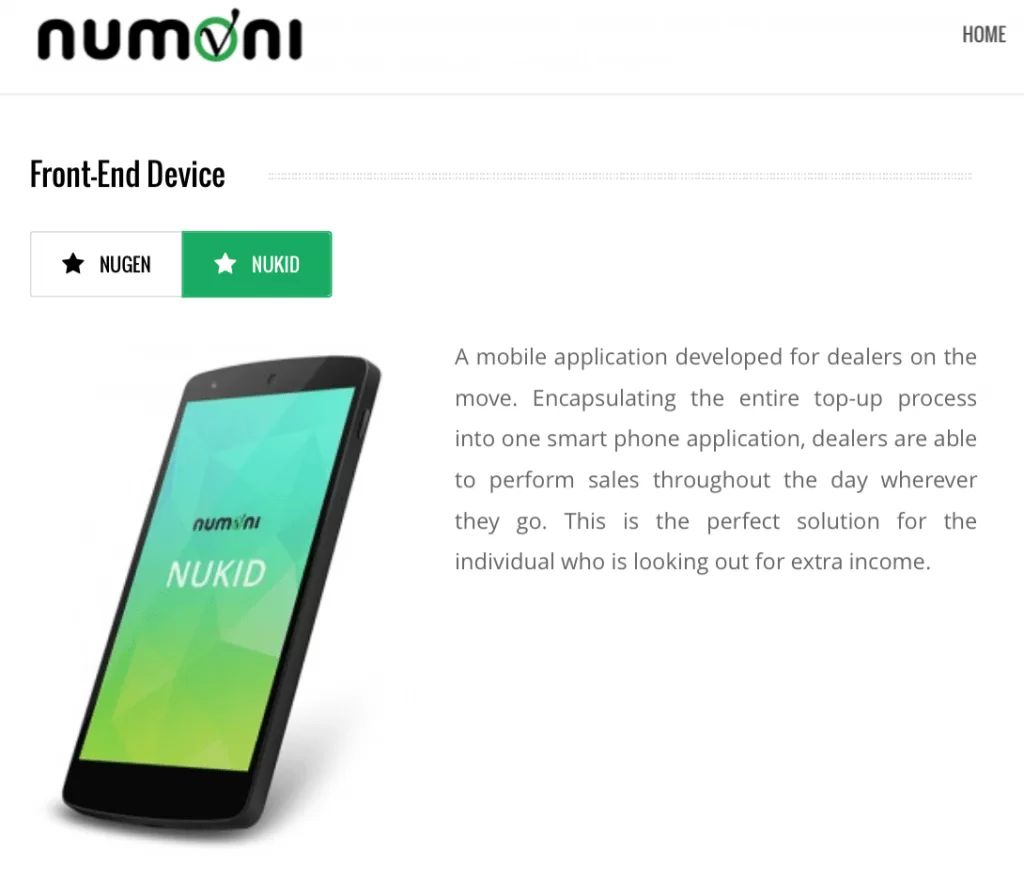

#2 NUKID

Basically a mobile app version of Nugen.

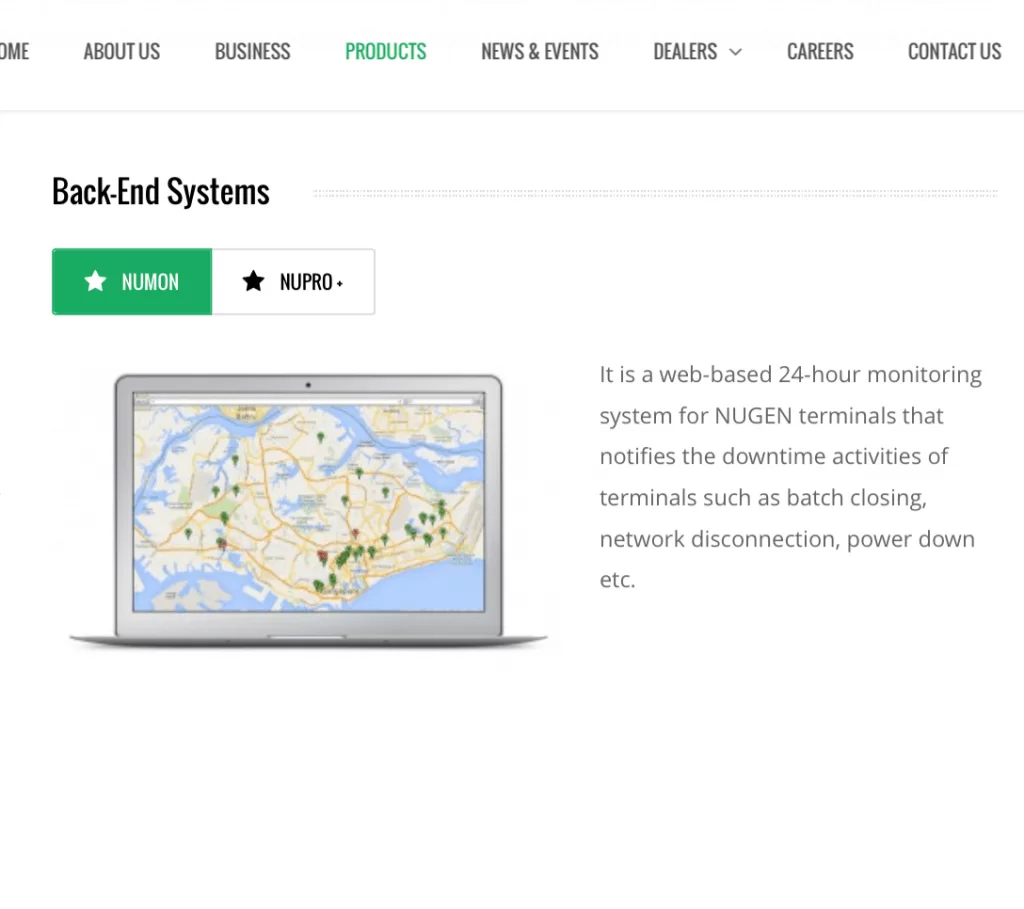

#3 NUMON

For buyers of NUGEN to monitor the terminals and ensure that they are functioning well.

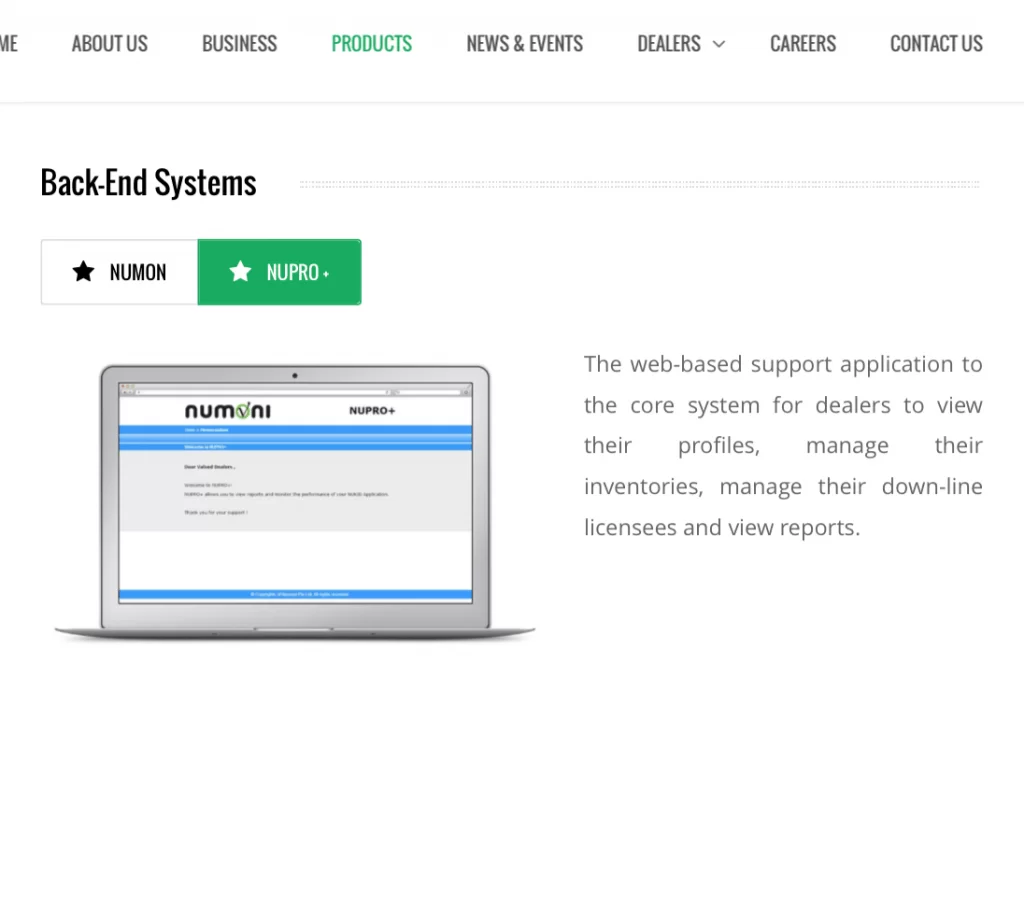

#4 NUPRO

A software application for Numoni’s dealers to organise their business and monitor their progress

Numoni was birthed from a desire to eradicate poverty, and that obviously involves a lot of finance. With technology, we are sure that Numoni’s mission will be achieved. All the best, Numoni!

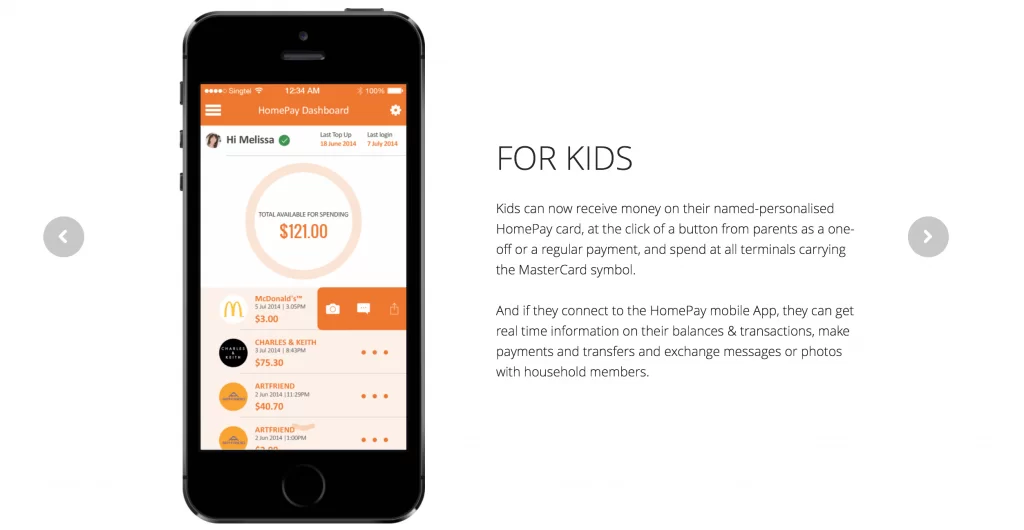

2. HomePay

HomePay is a mobile application for families interested in responsible and IT-savvy spending.

It presents itself as a provider of 4 assistances:

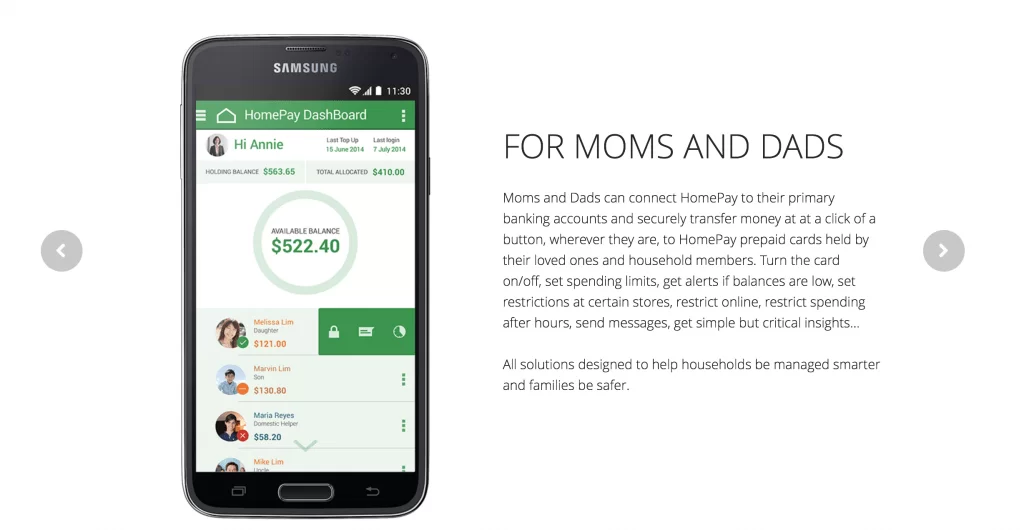

#1 Control

Users can set controls such as turning the card on/off, set spending limits, switch on alerts and restrictions on certain types of purchases, online payments and even time of the day.

#2 Insight

Users get real-time insights to what is being spent, weekly averages, where the card is being used on a map or even receive suggestions on how much should be transferred to kids and domestic helpers based on past spending.

#3 Conversation

Users can utilise the messaging and task features to converse with household members about household activities. Need money? How much? When? What is being bought? Or just a hello and a thank you.

#4 Convenience

Users can make money work smarter for their families. Sign up in minutes. Top up balances in a few clicks. Transfer money on the go. Be informed in real-time.

In the illustration below, you can see that Annie has real time information of her balance and the allocation amounts that she made into her daughter, son and helper’s HomePay accounts.

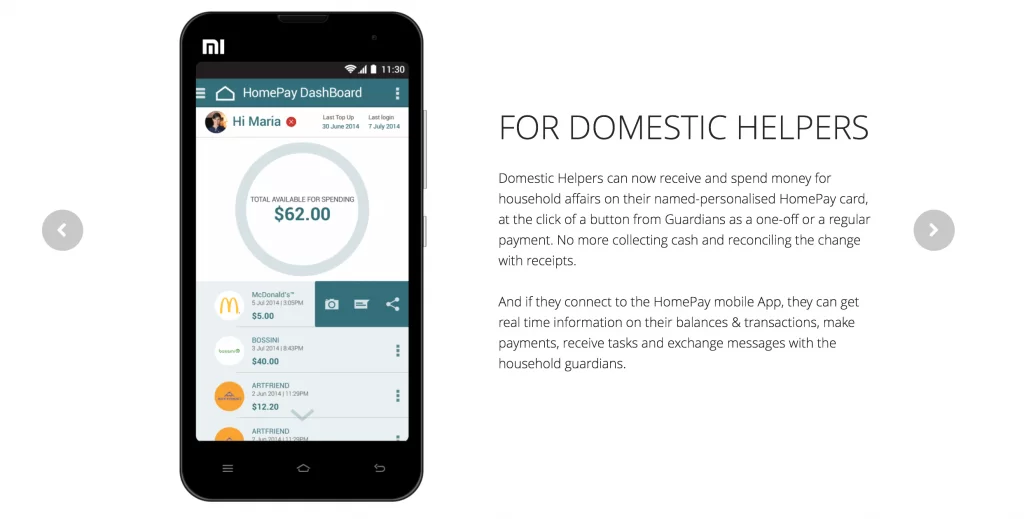

The amount that Annie allocates to Maria is reflected in Maria’s HomePay account. Her spending activities are reflected on the app too.

Same goes for Annie’s children.

HomePay offers families plastic or virtual HomePay MasterCard Prepaid Cards that can be topped up using the app and spent with all MasterCard approved Stores or online payment gateways.

HomePay has not been launched yet, but it is definitely a promising fintech product with many eyes watching it!

3. M-Daq

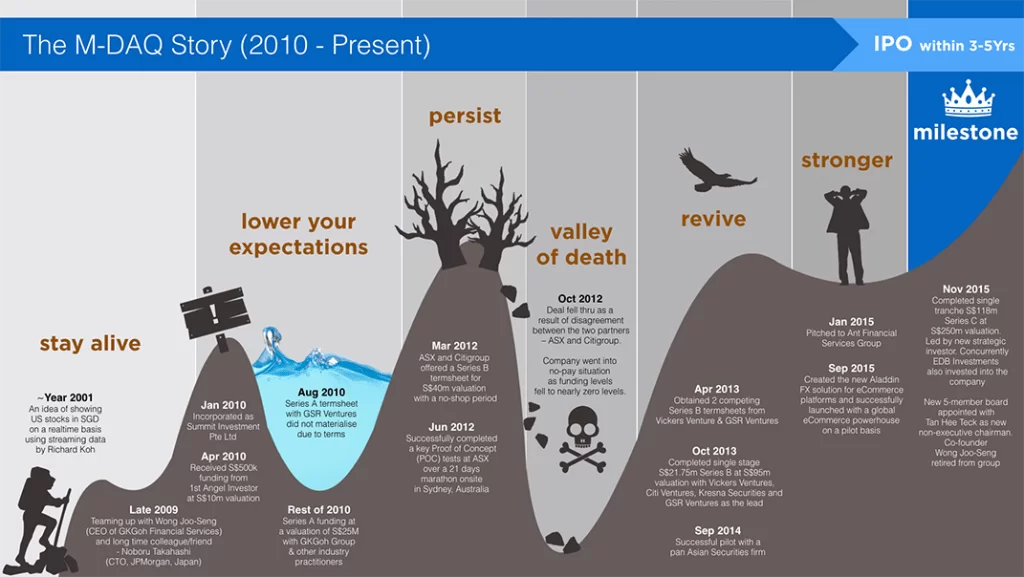

Infograph paints a thousand words:

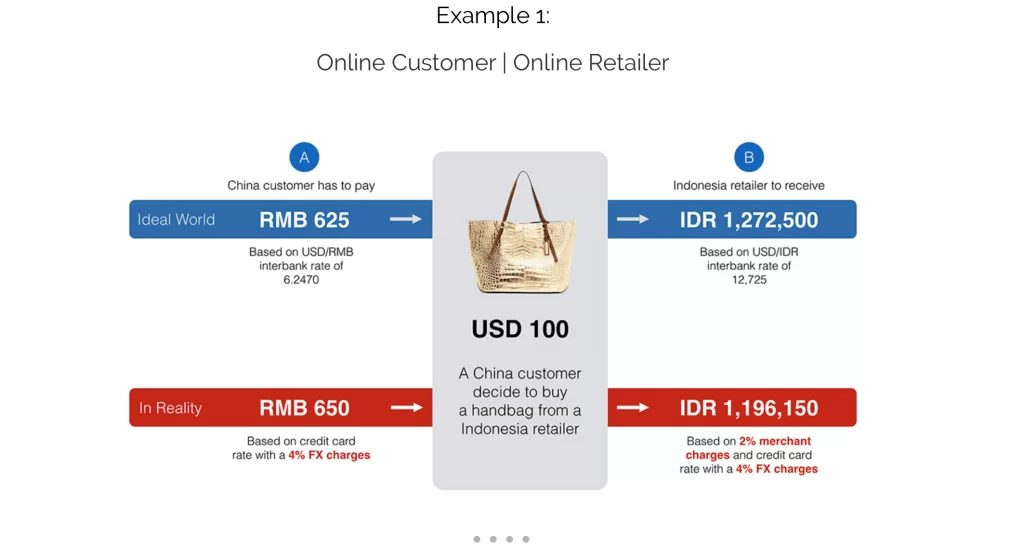

Basically, M-Daq’s innovation, in the form of a platform, an algorithm or a solution, enables dynamic multi-currency conversions for any cross border transaction which brings pricing certainty, transparency and savings.

It operates in three categories:

#1 Global markets – Multi-currency securities exchanges

This platform is able to price and trade exchange-traded products in a multitude of choice currencies, by blending FX rates into equities and futures products.

You and your clients can price, trade and settle exchange-traded products in a preferred currency, without fragmenting the underlying security liquidity pool.

Investors can price, trade and settle exchange-traded products in their preferred currency, with live pricing streamed via top 10 FX liquidity providers.

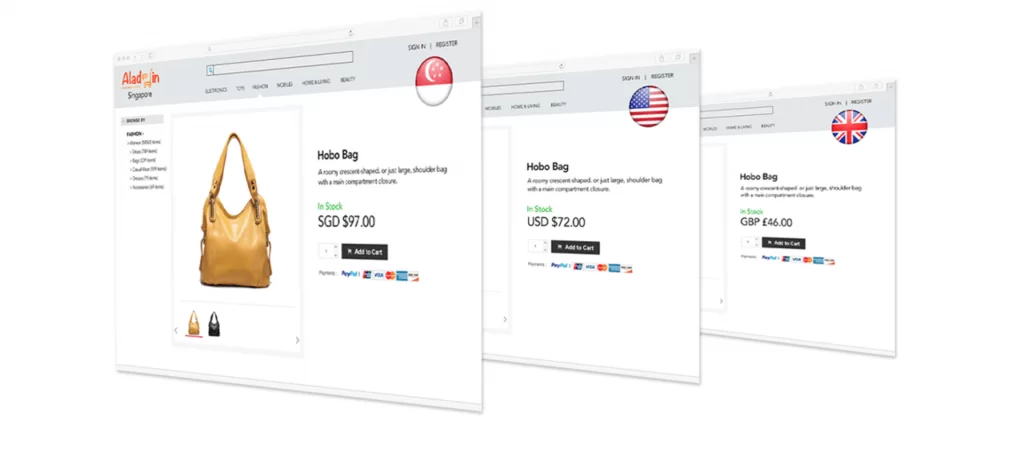

#2 E-commerce

Aladdin was created in September 2015 when the company took its innovative solution into eCommerce.

M-DAQ guarantees static or dynamic lock-in FX rates to price foreign goods in local currencies, protecting merchants against FX risk, among other functions.

Its solution makes it easier and risk-free for merchants to offer local prices to their online global customers, without the consumer needing to leave their eCommerce platform to check for external exchange rates, and therefore impacting the sales conversion rate.

With M-Daq, eCommerce businesses are expected to:

1. Increase Sales Conversion

2. Seamless FX Execution

3. Guaranteed FX Rates

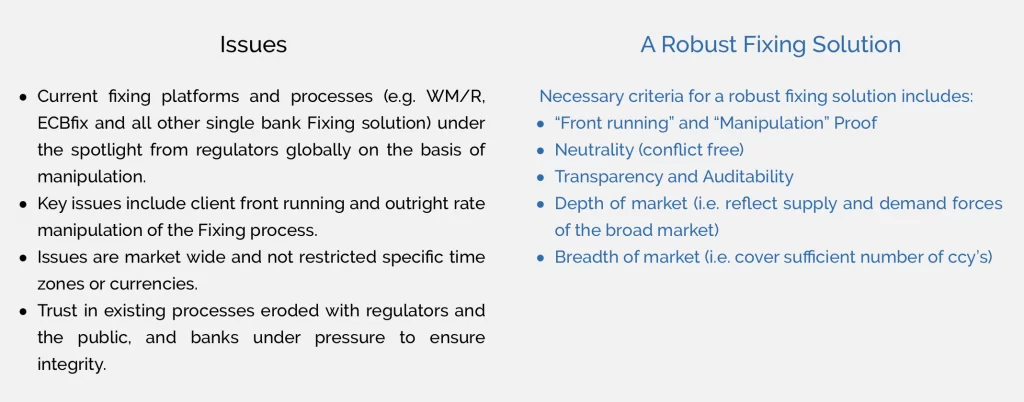

#3 Foreign exchange benchmark

M-Daq aims to provide an “Unbiased Best Execution” FX Benchmark Solution.

Its patented VWAP-Stacked price sourcing algorithm eliminates any possibility of rates manipulation and front-running by individual banks.

The algorithm determines the equilibrium supply and demand prices in isolation from both banks and fx traders, effectively decoupling how the rates are derived and how the positions are managed.

These prices are sourced from the core M-DAQ Securities Exchange Liquidity Pool where all FX Bank’s are streaming on a “no last look” basis, striving to maintain fixing prices that are competitive, neutral, transparent, manipulation proof and executable.

Isn’t M-Daq just impressive? Let’s just hope that it doesn’t end up like the next Ibis of Money Mon$ter!

Now that we have taken a peek at these three fintech companies in Singapore, let’s move on to hear what three experts have to say about fintech.

1. Vlab

Vlab is a global non-profit organization dedicated to connecting Silicon Valley’s entrepreneurs, industry experts, venture capitalists, private investors and technologists to enable them to effectively grow high-tech ventures amidst dynamic market risks and challenges.

A forum was organised last year, titled Fintech: Silicon Valley Takes On Wall Street, where spokespersons of fintech companies exchanged dialogues. You can find its video recording here.

These are some points mentioned by the four panelists in the 1 hour 20 mins video:

- Fintech’s focus is on technology, not profit from financial products or services.

- Fintech uses technology to simplify existing financial tools, making them mobile-friendly, user-friendly, and even beginner-friendly.

- Fintech digitalises the transactional activities of giving and receiving.

- Fintech acknowledges consumers of today who are more comfortable doing things digitally and are intolerant towards lack of transparency from financial institutions.

- Fintech bridges the experience gap between financial institutions and everything else which has already been mobilised.

- Fintech champions financial literacy with innovative products

2. OCTO Technology Suisse

OCTO Technology is an IT consulting, design, and implementation company that has been helping clients design information systems and applications, transforming their businesses since 1998. It focuses on technology, methodology and understanding business challenges.

From a slideshow that they have uploaded onto slideshare.com, OCTO reveals a thing or two about Fintech.

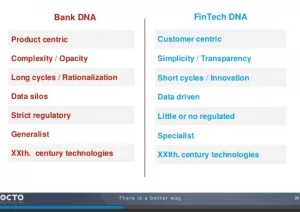

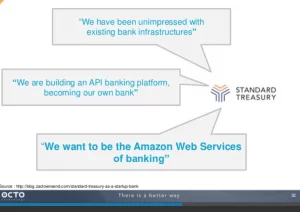

Firstly, there are fundamental differences between the traditional bank and Fintech.

Secondly, many Fintech companies are motivated by their unhappiness towards existing bank infrastructures, which are said to be products of the 1970s. There is much that technology can do in the Finance industry.

Thirdly, Fintech companies challenge banks to raise their standards on transparency and efficiency.

Currently, Fintech innovations are flourishing in the areas of Lending and Payments, followed by Personal Finance.

Yet, the grass is not entirely green on Fintech’s side. There is still much uncertainty about the growing sector.

3. Wall Street Big Names

Action speaks louder than words, so there’s nothing more assuring about fintech’s outlook than Wall Street bankers contributing to the US$17.8 billion investment in fintech, within the first nine months of 2015.

Six prominent names on the investment list are Vikran Pandit, former chairman and chief executive of Citigroup; John J. Mack, former chief executive of Morgan Stanley and Credit Suisse First Boston; Jon Winkelried, former president of Goldman Sachs; J. Christopher Flowers, former Goldman Partner; Hans Morris, former chief executive of Visa; and Joseph W. Saunders, also former chief executive of Visa.

Mr Morris explains that the purpose of investing in fintech is not to ruin the banking system, but to identify opportunities for technology companies.

Today’s generation of fintech companies are different. Many of the start-ups aren’t developing technology to sell to the financial services industry, as has been the pattern in past fintech booms.

Rather, they are taking their products directly to consumers through easy-to-use mobile apps and providing services that help consumers sniff out bargains and hidden fees in their financial dealings.

Bruce Wallace, chief digital officer at Silicon Valley Bank further explains that the public has taken to financial technologies after the financial crisis eroded its trust in the traditional banking system.

One concept that has captured a lot of attention is peer-to-peer lending, popularized by online sites like Prosper and Lending Club, which connect ordinary people who want to borrow money with ordinary people who are willing to lend it to them, cutting banks out of the process.

The lending sites flourished as banks curtailed unsecured and riskier lending.

Conclusion

I hope this article, with all these information about Fintech, hasn’t been an overwhelming read. And I hope that the information presented here has been helpful.

Indeed, Fintech is the next tech behemoth of our age and there is still much about Fintech that has not been said in this article.

If you are interested, and want me to write more about it, please comment below or send me an email at serene.chao@webimp.com.sg.

Meanwhile, go dream away about creating your own NUGEN, HomePay or M-DAQ solution!

Click here to read about the importance of having an online presence.